You cannot take control of your financial life if you don’t know two basic things: (1) how much money is coming in, and (2) how much money is going out. Most people operate in the dark as it relates to their finances. They often take the head-in-the-sand approach or the, cross-your-fingers and hope approach to their financial life. Yikes! Perhaps it will end up working out, but what a stressful way to handle your money.

Just knowing where your money goes and how much you need to “keep the lights on” at home provides a tremendous sense of relief. It is integral to everything related to your financial life. So, building a cash flow projection should be at the foundation of your financial strategy.

Rather than averaging expenses over a year, I advise that you project your annual income and expense by month. But don’t go over-board. It isn’t meaningful to create line items for coffee expenditures or even clothing for that matter. Rather, list all expenses that you need to keep your house running, food in the fridge and gas in the car. The rest is discretionary; it’s what you can spend on things like eating out, movies, clothes etc.

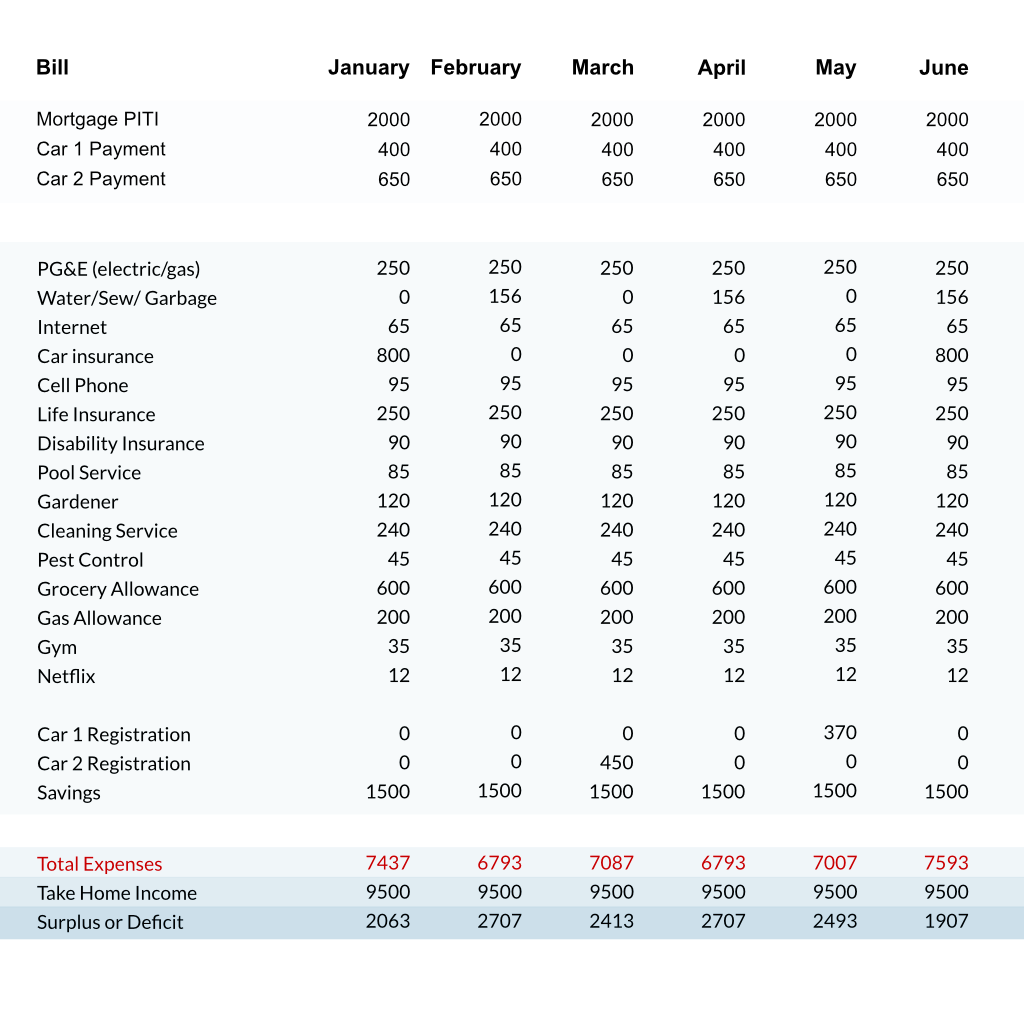

I use Excel for my projections, so I don’t have to calculate these by hand. It looks like this, but for a whole year:

Identify & Prepare: Remove your head from the sand!

Knowing your expenses by month, allows you to identify and prepare for the months when expenses are going to spike; for instance, when car registration or insurance is due. It forewarns you that discretionary spending will have to go down for that month. I call those, ‘frugal’ months in my domestic life.

Simply averaging the expense over the year doesn’t tell you everything you need to know. If you outline your specific monthly expenses, you will more easily control where the money is going.

Notice too, that I include a line item for savings. Because you are using your “take-home” pay in in the calculation, you wouldn’t include savings that goes into your 401(k). However, most people need to save more than just what goes into their 401(k) and so that’s where this line item belongs.

Trim Excess: Find money buried in your budget!

Also, seeing your expenses listed helps you to find more opportunities to save! Once you can clearly see exactly where the money is going, look for unnecessary expenses or where you are overpaying. Call your cell phone company and find a less expensive plan, reduce your monthly TV expense by cutting channels you don’t watch, or cut the cable altogether and utilize streaming.

Customize: Make it yours!

If you are trying to pay off a debt sooner… add it to this projection. Create a line item for accelerated debt pay down.

Use your projection to measure the impact of an additional expense. If you are thinking of buying a new car, for instance, and intend to have a larger car payment… plug it in to your spreadsheet in advance to see how it will affect each month.

The point being, once you unveil the mystery of your spending, you can control the money and start meeting your broader financial goals. Whether you want to save more money or pay down debt, it all starts with knowing how much is coming in and how much is going out.