Taxes rarely become simpler over time, and the One Big Beautiful Bill is no exception. Signed into law on July 4, 2025, the legislation introduces a mix of expanded deductions, temporary tax breaks, and new income phaseouts that could meaningfully affect many working and retired families over the next several years.

For some households, the changes may create valuable opportunities to reduce taxes. For others, they may introduce new planning challenges and unexpected complexity.

The reality is that many middle- and upper-middle-income families are already balancing rising property taxes, higher incomes, retirement savings decisions, charitable giving, and increasing living costs. This legislation touches nearly all of those areas.

Some of the most important changes include:

- a significantly larger SALT deduction for certain taxpayers,

- new deductions for seniors,

- a new deduction for auto loan interest,

- and updated rules surrounding charitable deductions and itemized deductions.

At the same time, many of these benefits begin disappearing once income crosses certain thresholds, creating situations where thoughtful planning may matter more than ever.

In other words, this bill is not simply about paying less tax. It is about understanding where opportunities exist, where deductions begin to phase out, and how even small planning decisions could potentially save families thousands of dollars over the next several years. Following are a few noteworthy changes as a result of the OBBB:

1. The Standard Deduction Is Higher

The standard deduction remains elevated and was increased for 2025 and 2026 to:

Filing Status

Married Filing Jointly

Single

Head of Household

2025 Standard Deduction

$31,500

$15,750

$23,625

2026 Standard Deduction

$32,200

$16,100

$24,150

Example:

A married couple with mortgage interest, property taxes, and charitable gifts totaling $28,000 would still likely take the $31,500 standard deduction because it is higher. This means their charitable gifts may not provide an additional tax benefit unless they itemize or use another available charitable deduction strategy.

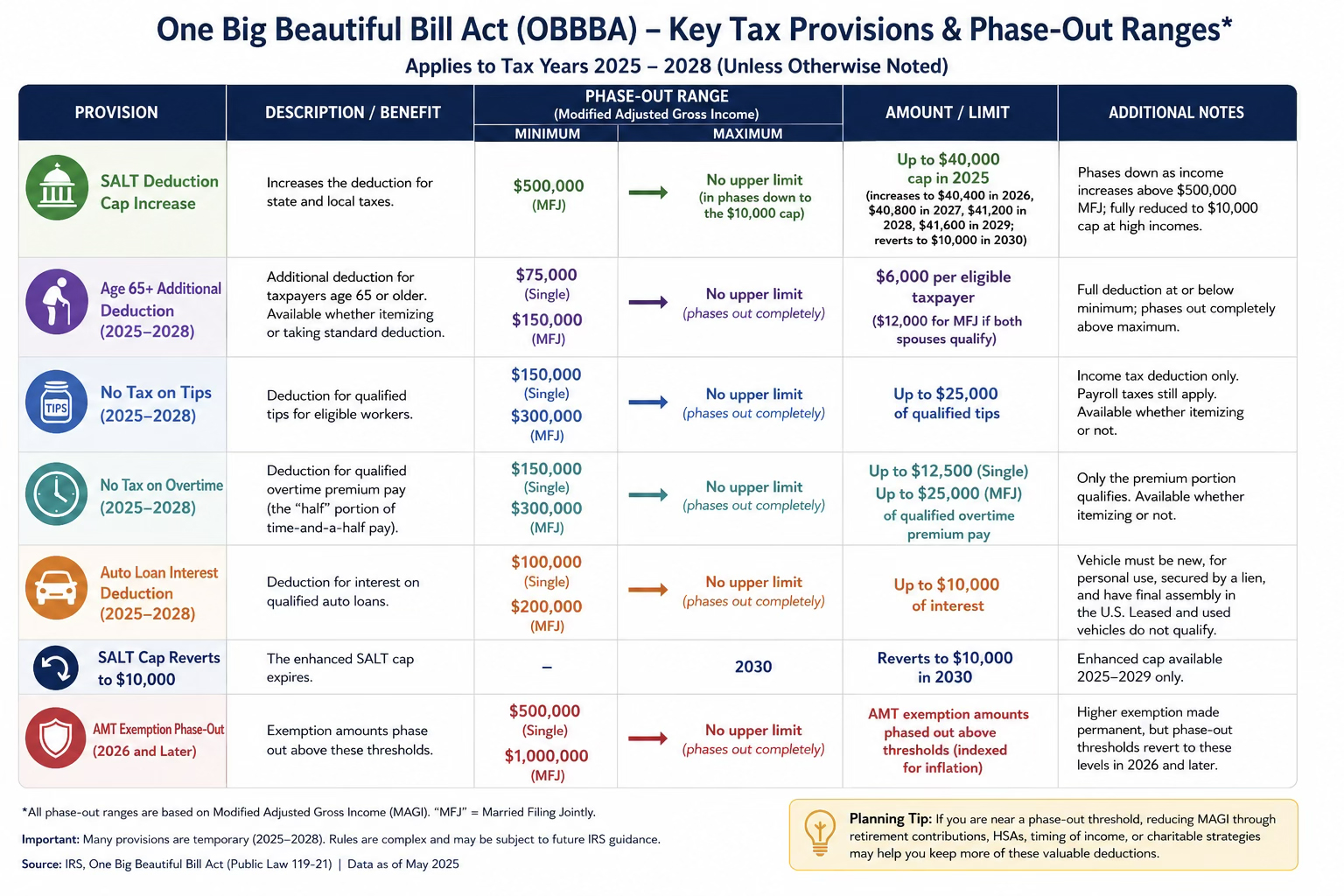

2. The SALT Cap Temporarily Increases

The deduction for state and local taxes, often called the SALT deduction, increases from $10,000 to $40,000 beginning in 2025. This is especially meaningful for families in higher-tax states with significant property taxes and state income taxes. The cap increases slightly each year through 2029, then returns to $10,000 in 2030.

Example:

A California couple pays $18,000 in property taxes and $22,000 in state income taxes. Under the old $10,000 cap, only $10,000 was deductible. Under the new $40,000 cap, the full $40,000 may be deductible, assuming they are not phased out.

3. The SALT Cap Has an Income Phaseout

The higher SALT cap begins phasing down when modified adjusted gross income exceeds $500,000 for joint filers. It phases down toward the old $10,000 cap for households with higher income.

Example:

A family earning $475,000 may receive the full benefit of the $40,000 SALT cap. A family earning above $500,000 may begin losing part of that enhanced deduction. This creates a planning opportunity around retirement contributions, deferred compensation, charitable bunching, and other income-reduction strategies.

4. AMT Planning May Matter Again for Some Families

The Alternative Minimum Tax, or AMT, never went away, but fewer families were affected after 2017. The OBBB makes the higher AMT exemption permanent but also reverts the exemption phaseout to $500,000 for single filers and $1,000,000 for joint filers in 2026, indexed thereafter.

Practical point:

Families with high income, large state taxes, incentive stock options, or significant deductions should continue to run AMT projections before year-end.

5. Charitable Giving Rules Become More Layered

Beginning in 2026, taxpayers who itemize may only deduct charitable contributions to the extent total giving exceeds 0.5% of AGI.

Example:

A family with $400,000 of AGI gives $5,000 to charity. The first $2,000, equal to 0.5% of AGI, does not count. Only $3,000 is potentially deductible.

This makes charitable contribution strategies more important. Families may benefit from bunching several years of charitable giving into one tax year, using a donor-advised fund, donating appreciated stock, or coordinating gifts with unusually high-income years.

6. Charitable Deduction for Non-Itemizers

Beginning in 2026, taxpayers who do not itemize may still deduct charitable gifts up to $1,000 for single filers and $2,000 for married couples filing jointly.

Example:

A married couple takes the standard deduction but gives $2,000 to qualified charities. They may still receive a charitable deduction even though they do not itemize.

7. Itemized Deduction Limit for High Earners

Beginning in 2026, taxpayers in the 37% bracket (income exceeds $640,600 for single taxpayers and $768,700 for married couples filing jointly) may see the value of itemized deductions effectively capped at 35%.

Example:

A high-income taxpayer donating $10,000 may not receive the full 37% tax benefit. Instead, the benefit may be closer to 35%, reducing the tax savings from about $3,700 to about $3,500.

8. Additional Deduction for Some Taxpayers Aged 65 and Older

From 2025 through 2028, taxpayers aged 65 and older may claim an additional $6,000 deduction per eligible person. A married couple where both spouses qualify could receive up to $12,000. This deduction is available whether the taxpayer itemizes or takes the standard deduction. It phases out when modified AGI exceeds $75,000 for single filers and $150,000 for joint filers.

Example:

A retired married couple, both aged 67, with income below the phaseout threshold may receive an additional $12,000 deduction on top of their standard deduction and existing senior deduction.

9. “No Tax on Tips”

From 2025 through 2028, eligible workers may deduct up to $25,000 of qualified tips. The deduction phases out when modified AGI exceeds $150,000 for single filers and $300,000 for joint filers. It is available to both itemizers and non-itemizers.

Important:

This is an income tax deduction, not a complete exemption from payroll taxes.

10. “No Tax on Overtime”—Read Carefully, It Is Misleading

From 2025 through 2028, eligible taxpayers may deduct qualified overtime compensation up to $12,500 for single filers or $25,000 for joint filers. The deduction applies only to the overtime premium portion, such as the “half” portion of time-and-a-half pay. This deduction phases out between $150,000 for single filers and $300,000 for joint filers.

Example:

An employee earns $30 per hour and receives time-and-a-half, or $45 per hour, for overtime. Only the extra $15 per hour premium may qualify for the deduction.

11. Auto Loan Interest Deduction

From 2025 through 2028, taxpayers may deduct up to $10,000 of interest on a qualifying auto loan. The vehicle must be new, purchased after December 31, 2024, for personal use, secured by a lien, and have final assembly in the United States. Leases and used vehicles do not qualify. The deduction begins phasing out at $100,000 of modified AGI for single filers and $200,000 for joint filers.

Example:

A married couple buys a new qualifying SUV assembled in the U.S. and pays $3,500 of auto loan interest in 2026. If their income is below the phaseout threshold, that interest may be deductible.

Final Planning Takeaway

The OBBB creates real tax savings opportunities, but many are temporary, income-limited, or dependent on whether a taxpayer itemizes. For many families, the best planning opportunities may come from timing income, bunching charitable deductions, reviewing SALT exposure, coordinating retirement contributions, and taking advantage of the temporary 2025–2028 deductions while they are available.

At Whelan Financial we are here to work with your CPA to help navigate these complexities and planning opportunities for you.

Authored by Whelan Financial

Preliminary language, parameters, and edits for this blog were crafted by the Whelan Financial team, with the help of generative AI.